Introduction

One of the themes I have been trying to drive home in many of my articles is that a key component of value acceleration involves growing both the absolute amount of cash flow in your business as well as its sustainable growth rate. This is important because in the end, size does matter when it comes to valuation. This article will illustrate how there are various valuations tiers in the Middle Market and why it is advantageous for a business to grow itself into the next tier.

Pricing Tiers

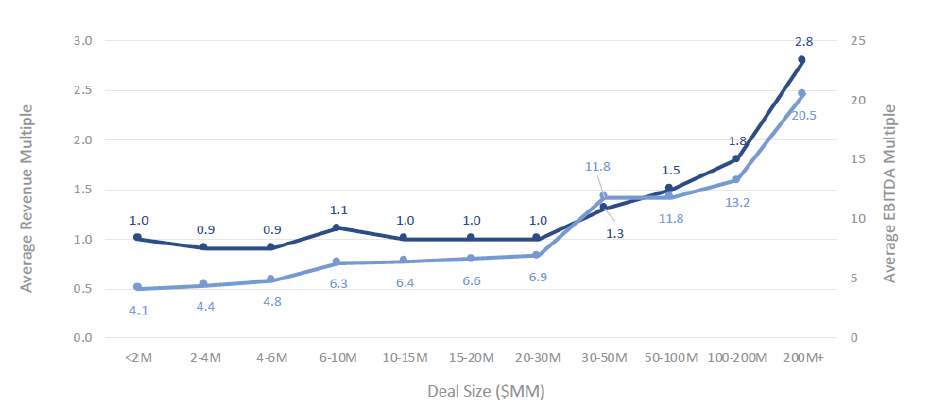

In the exhibit below (courtesy of the Association of M&A Advisors), EBITDA pricing multiples are shown and compared to deal size (measured in Enterprise Value). These multiples were sourced from the 2020 Q2 Deal Survey conducted by the AM&AA. As can be seen, there is a positive relationship between deal size and the EBITDA multiples. More accurately, we can see the multiples do not increase gradually like a straight line but rather in a step-up fashion. Based on this data, there is four distinct tiers:

- $6 million and less;

- $6 million to $30 million;

- $30 million to $200 million; and

-

$200 million or greater.

Exhibit 1 – Deal Size vs. Multiples

Source: AM&AA DealSurvey 2020 Q2

Each of these tiers demonstrates a distinctive range for cash flow multiples*. As transactions approach the next tier, the multiple range “jumps” to the next level. For example, most “main street” companies (with enterprise value of $6 million or less), tended to transact in EBITDA multiples in the 4x range. However, the next tier above (what would be the Lower Middle Market here in Canada), multiples increase into the 6x area. The next tier above that (for lack of a better term, we can call it the Middle Middle Market), multiples rose to the 11x range. Finally, when we get to the Upper Middle Market, multiples start to resemble public company cash flow multiples.

Why do these tiers exist? For the most part, each of the tiers represents categories of companies with a unique group of potentially interested buyers. As the enterprise value of the company increases (and thus cash flows are increasing as well), more prospective buyers are interested in purchasing that business. For example, for companies with enterprise value of $6 million or below, the likely pool of buyers includes mostly other competitors or investor/entrepreneurs seeking business opportunities. Such buyers are mostly going to be financial buyers, with perhaps only a small portion of prospective buyers that could be classified as strategic in nature. In the next tier up, the pool of prospective buyers increases to include private equity (which could include PE firms, family offices, and independent sponsors). A small portion of prospective buyers would include public companies looking to expand geographically, horizontally, or vertically. While many companies would be financial buyers, the percentage of strategic buyers would grow here. Moving onto the next tiers, the percentage of larger PE firms and public companies in the prospective buyer pool increases. PE firms here have more financial muscle and may be seeking bolt-on acquisitions. Many public company acquisitions would also have some degrees of synergistic value.

To summarize, as the enterprise value of the business grows:

- The pool of prospective buyers increases;

- The financial muscle of these prospective buyers increases;

-

The proportion of prospective buyers who are strategic or synergistic buyers increases.

All three of these characteristic help to propel higher multiples

Key Takeaway

What does this mean for the average Middle Market business owner? This illustrates the potential importance of growing the absolute size of the company along with adopting a sustainable growth strategy. As can be seen, it can significantly elevate the potential selling multiple and it also offers the business owner a greater number of options to transition from their business. More money and more options is always a good thing.

*A quick caveat about the multiples here. I am showing these multiple to illustrate a point, however, there are many factors which go into the multiple of a business including its growth rate, financial performance vs. peers, and overall perceived risk specific to the company. Generalizations cannot be made here about what a company might be worth solely based on its size. Rather, a detailed valuation should be performed to assess multiple factors that go into the valuation of a business. Also note that the “main street” category of $6 million EV or less is a broad one that includes many smaller companies under a million dollars with lower multiples ranging from 1x to 3x. Lastly, I’ll remind everyone that the observed multiples in the marketplace are from deals that actually transacted. The majority of businesses listed for sale do not sell. The valuation of a business that cannot sell is its liquidation value.