Key Takeaways

· For many business owners, personal and business wealth are tightly correlated.

· Business owners should devise a plan (and execute upon it) for each of the five stages of Value Maturity to maximize their personal and business wealth.

· To optimize results, the five stages should be addressed in order.

(The Value Maturity Index is copyrighted by the Exit Planning Institute and is used with permission.)

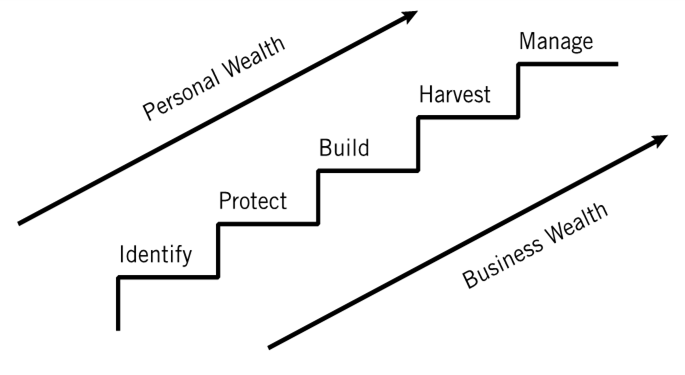

The Five Stages of Value Maturity

Value maturity refers to a process in which a business owner adopts a value creation mindset and nurtures the value of their business over time with the expectation that the value of the business will eventually be harvested. The steps of Value Maturity are logically followed in a sequential order since harvesting value cannot be optimized by skipping earlier stages in the process. Below, we briefly describe each stage of Value Maturity.

Identify

The very beginning of the value acceleration process is to take time to properly identify the value drivers, and more importantly, the gaps within your business because this lays the foundation for you as an owner to start to potentially increasing your business’ value. There are three main gaps an owner should consider: income gaps, value gaps, and wealth gaps. These can be defined as follows:

i) Income Gap—The gap between what a business generates in cash flow versus what industry peers earn;

ii) Value Gap—The gap between what a business is worth today versus what it can potentially be worth if improved by addressing key value drivers;

iii) Wealth Gap—The gap between what wealth an owner has now (on an after-tax basis once his business value has been harvested through a sale, transition, or liquidation) versus what wealth would be required for that owner to enjoy a standard of living they desire upon retirement.

Each of the above gaps are important to identify since every business owner has a vested interest in minimizing those gaps before the eventual sale, transition, or liquidation of their business. Understanding all three is important but it is truly the wealth gap that drives the need to understand the value gap (since the value of the business will determine an owner’s wealth upon exit), and the income gap can play a major role in determining the valuation gap (since the primary driver of business value is the cash flows it generates). Thus, to address the wealth gap, one must first address the value gap, and to address the value gap, once must first address the income gap. In this sense, each of the gaps are inter-related.

There are other factors that are also important to understand at the identify stage. For example, to what degree is an owner ready to exit their business from a personal level (irrespective of finances and wealth)? Is the owner truly ready to let go of their ‘baby’? Is the owner motivated to keep growing the business rather than relinquish control? Does the owner have any post-transition plans in place to fulfil themselves? For many owners, there is a thin separation between their business and personal lives and is a key part of their identity. Failure to identify and later address these matters can result in either 11th hour cold feet when transitioning a business or serious regret upon exit. This can be avoided if care is taken at the beginning stages to address personal readiness matters.

In general, the objectives of the ‘identify’ stage are threefold: Assess

i) the business readiness of your Company to be transitioned;

ii) your financial readiness to retire comfortably; and

iii) your personal readiness to transition away from your current business.

Through clarifying the above three objectives, an owner is now in a position to set their own roadmap to exit, through taking a holistic approach.

Protect

One of the main components of the value acceleration methodology is the de-risking of your business. By de-risking a business, you can inherently increase the value of it. While de-risking is sometimes perceived as less glamorous, in actuality it is the step that can lay the foundation for future growth and an increased value of the business upon transition. Given all this, how can an owner go about protecting their business?

1) Systemic Documentation

Transferability and repeatability are two of the key tenants to value creation. Transferability means that the “secret sauce” of the organization is not simply stuck in the head of the owner, who when removed from the situation, the business suffers, or worse, fails. Repeatability refers to the ability of an organization to repeat a successful process over and over again, even when there is employee turnover. Repeatability allows the business to take on a life of its own separated from the owner and senior management. Both of these can be achieved through proper documentation of processes within the organization. Processes could include functional areas such as sales, manufacturing, operations, finance, human resources, information technology, marketing, and of course, related to any intellectual property development performed by the company. Documentation allows for consistency and teachability throughout the organization. Without it, the organization’s knowledge is concentrated in too few individuals and if anything happens to them (due to bad health or having to leave the organization), the knowledge accumulated may forever escape from the organization. This is a threat to an organization’s valuation and potentially its long-term existence, which is why the systemic documentation process is a key element of de-risking.

2) Financial and Operational Insight

If you are heading out on a road trip, you need to know both where you are going and how to get there. You’d probably like to know if a certain road is closed, forcing you to take a detour. You might also like to know how heavy traffic will be at certain locations to minimize traffic jams. Similarly, operating a business is often like a road trip (commonly with scenic route side trips attached). With any road trip, you need visibility to avoid obstacles in your path. For an organization, having financial and operational insight is critical.

Financial insight refers to the ability to see an organizations cash flows into the future so that they can be managed effectively given the size and growth rate of the organization. This should include the ability to budget (at least annually) and perform a twelve-month rolling forecast for not only operations, but taking into considerations investments in working capital, capital expenditures, debt repayments (both interest and capital), dividends, taxes, project financing, along with a contingency amount for unforeseen circumstances. If your company has third-party debt with covenants attached, being able to foresee cash crunches or going offside of these covenants can give you a heads up when dealing with the lender. Even a debt free company still needs to understand how its cash flows are working especially one that is growing fast since top line growth doesn’t always translate into increased cash flows. Financial insight will also give you the ability to assess how profitable each customer is and whether they are meeting minimum thresholds that are truly creating value for the company. (Some customers may have terms so bad you are actually destroying cash every time you make a sale to them!)

On the operations side, insight into customer demand, supplier constraints, and manufacturing capacities can help your organization optimize production and avoid bottlenecks either in your supply chain or your warehouse. Increasing sales is desirable but if you can’t keep up with demand, any increase in revenues will be short-lived as you only serve to frustrate customers. Similarly, better insight into operations will allow for reduced costs since waste and inventory costs will be minimized.

Being able to forecast the future with reliability can help a business avoid having to become reactionary to seemingly random events when with some planning, issues can be avoided or minimized, and contingency plans can be made.

3) Contingency Plans

The more transferrable a business, the less it relies on its owners. Part of creating this transferability is through an owner creating a contingency plan. A good contingency plan should incorporate:

· Insurance for shareholders and key employees to manage the process of a voluntary or involuntary departure from the business along with appropriate insurance for the company.

· Competitive compensation plans for key employees to keep their interests aligned with those of the business owner (and keep them loyal to the organization).

· A detailed shareholder’s agreement that manages the process of a shareholder having to be bought out due to:

o Dispute with the other shareholders;

o Divorce of a shareholder;

o Death of a shareholder; or

o Disability of a shareholder;

· A disaster recovery plan.

4) Business Operating System/Infrastructure

The larger a company grows, the more complex are the interrelationships between employees and management. When businesses start, often the owner wears multiple hats and has a hands-on role in all functions. However, part of moving from a small business into the middle Market requires hiring key functional personnel in the functional areas of human resources, finance, operations, sales, marketing, and IT. The old ways of running the business cease to work and a business operating system is required to establish processes within the organization and a rhythm for communication. Part of growing a business is also predicated on providing infrastructure to support these processes and enable organizational growth.

5) Diversification of Customers/Suppliers

A business that is too reliant upon one customer or supplier is at a competitive disadvantage compared to more diversified businesses. If that customer leaves (or goes out of business), the company may experience a major decline in revenues. Similarly, relying too much on one supplier can put the organization in a position where it may be subject to unforeseen price increases or have its supply chain break down rapidly if the supplier gets into financial trouble.

Grow

Once the owner has adequately de-risked their business and added in the necessary infrastructure and processes, they are now ready to grow the business. Because of your previous work, the infrastructure is now hopefully there to support the growth in this next stage, which is the value creation stage. The growth stage is more complicated but is the area in which the owner now concentrates on growing EBITDA and developing intangible assets. This is the stage where the multiple for one’s business can really be expanded if the execution is on point. This stage is also much more strategic than the previous one since it involves the owner devising ways to grow cash flow and potentially re-imagine their business through planning out new revenue streams.

Growing EBITDA

Growing EBITDA requires a move away from focusing less on top-line growth and more on building sustainability and visibility. This means landing customers who provide longer-term value and positive impacts on the bottom line. Growing EBITDA also requires prudent management of working capital and, for capital intensive industries, a solid capital budgeting process. Cash flow can be grown through finding new customers or expanding business with existing customers. Since finding new customers can be a time and resource-intensive process, the latter may ideally prove the be the best path to growth, but this will depend largely on your business model and the growth stage of your company (start-up, growth, or mature).

New Revenue Streams

The growth stage requires a strategic rethinking of your company. How best can growth be acquired? Some companies choose to focus on doing one thing extremely well (and achieve growth through customer loyalty and organic growth through word-of-mouth and advertising), while others achieve growth through being creative in finding new revenue streams. This may include finding natural add-ons to existing services based on customer feedback or expanding into complimentary products and services. Sustainability is also important. This was one reason many software companies moved from a buy-an-upgrade model to a software-as-a-service (SaaS) model which provides month after month of recurring revenue.

Organic versus Engineered Growth

Growth can be achieved either organically (through using internal resources to increase revenues) or engineered through merger & acquisitions. The reality today is that many large public and private companies achieve growth through M&A, either expanding their existing business geographically, vertically (for example buying out a key supplier to achieve synergies), or horizontally (expanding into complimentary products and services offered by an industry competitor). Advanced value creation will likely always involve some degree of buy-side M&A strategy that will require owners to understand the purpose of the acquisition, buying at the right price, understanding synergies, and developing a post-implementation plan.

Harvest

For every business, there is a time to harvest the value that has been created throughout its lifetime by the owner and management. Exits may be involuntary (due to death of a shareholder, shareholder dispute, divorce, owner disability, or distress that results in a liquidation of the company’s assets). However, value is more likely to be maximized when the event is planned out in advance. Common exits may include:

· Sale to a third-party company;

· Private equity investment (either majority or minority stake);

· Management buy-out;

· Employee Stock Option Program (ESOP);

· Transition to a family member; or

· Some hybrid of the above.

The attractiveness of any exit option will depend largely on the owner’s objectives. For example, for an owner seeking a maximization of after-tax proceeds, selling the business to a strategic buyer (if any exist) might be the optimal route. However, other factors such as family legacy might play a much larger role than simply money. Also, a key variable in the mix is what does the owner wish to do with their post-exit life? Does it include a complete exit from the business? Merely stepping back and acting like a chairman of the board? Does it include rollover equity and a piece in future profits generated from a separate management team?

Management

Once the Harvest stage is complete, the owner is now focused on managing the after-tax wealth extracted from exiting their business. This wealth management may take form in multiple ways:

i) Invest and retire;

ii) Philanthropy;

iii) Re-invest in a new business and manage it;

iv) Join or form a Private Equity Group/Family Office; or

v) A hybrid of the above.

There are many options at this stage but understanding your preferences well before the exit will ensure your exit strategy is aligned with your personal goals.